We’ve updated our targets: here’s why

In a recent post here, we talked about the work we do to model pathways to net zero, and why this matters.

As the world changes around us, our plans, targets and pathways also need to adjust – in some cases to reflect a new reality, and in some cases to improve or add detail that makes targets more actionable.

In our 2024 annual report, we announced new targets and pathways for sea, road and terminal activities. This update is partly to re-align with the latest climate science, and partly to provide more guidance for our operations to act in support of our decarbonisation ambitions.

Old targets and new

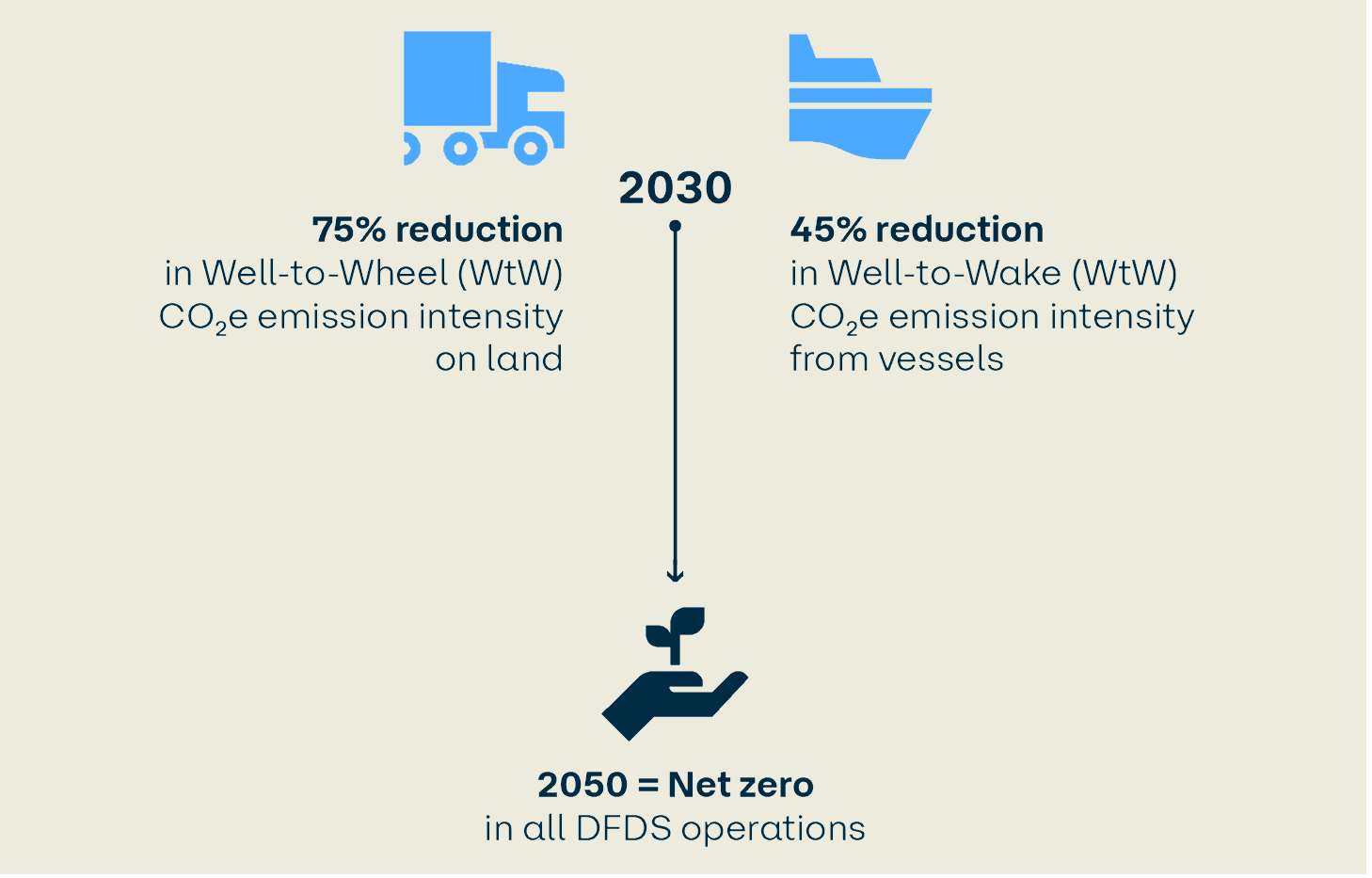

DFDS has previously communicated two distinct 2030 targets, and a 2050 target of net zero greenhouse gas emissions.

The 2030 target for vessel activity was based on old guidance from the International Maritime Organization (IMO), and stated a 45% reduction in Tank-to-Wake CO2 emissions intensity, from a 2008 baseline. This is out of step with our targets for land activity, which were set more recently. Our land target remains a 75% reduction in Well-to-Wheel CO2e intensity from a 2022 baseline.

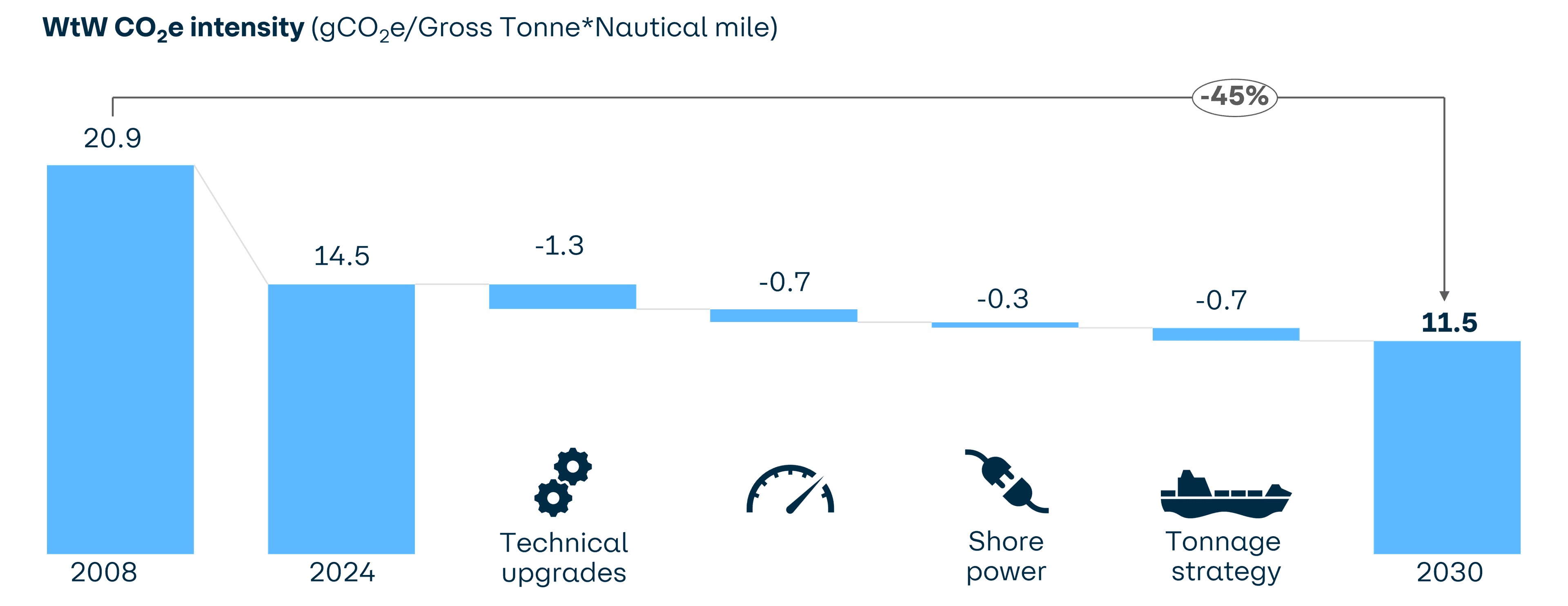

So the first big update is that we have changed our vessel targets to cover all greenhouse gases, and to include the Scope 3 emissions related to our fuel. In other words, we have updated the target from TtW CO2 to WtW CO2e. The 45% reduction in emissions intensity still applies, but because it is calculated on a broader scope of emissions, the pathway for vessels has also been updated.

Included in the new pathway are the FRS vessels acquired in 2023, and the contribution from shorepower projects to emissions reductions in port. The tonnage strategy consists of the introduction of new, low-emission vessels as well as the decommissioning of older vessels.

Absolute emissions and emissions intensity

It may seem counter-intuitive that our targets are all based on emissions intensity, when we all know that the goal is to reduce absolute emissions. The reason we use intensity is to be able to keep our targets consistent regardless of growth and acquisition. If we acquire a new route, then technically we would acquire a new portion of greenhouse gas budget associated with this route. In terms of absolute emissions, this would mean recalculating a baseline (where data might not be available), and then recalculating a new target. But when we stick with emissions intensity, the targets don’t change – regardless of whether we acquire routes with a higher or a lower intensity than we have today.

Pathways to drive progress

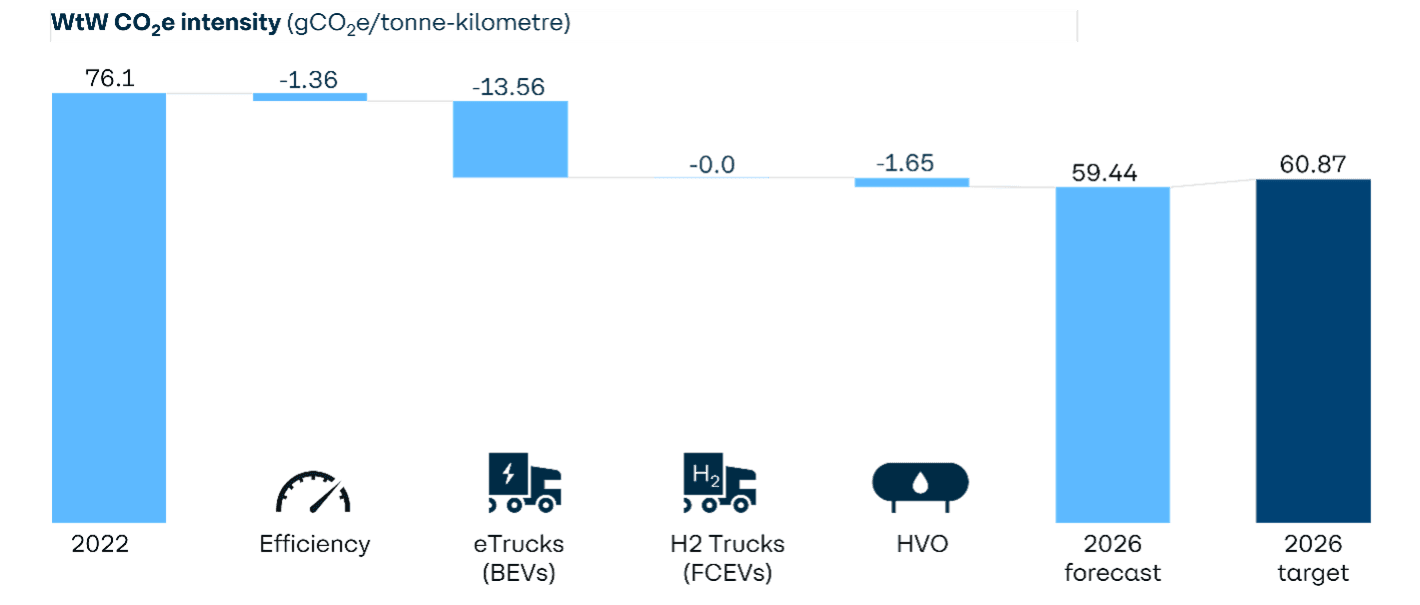

It’s all very well having big and long-term targets, but how do we make these more tangible, and more actionable? Behind the scenes, we break down our targets into annual goals, across our different operational activities. At this point, the focus shifts from setting targets to establishing rather concrete, short-term pathways to deliver against those targets. As an example, here’s an early version of our 2026 pathway for road (to read more about finding pathways in decarbonising DFDS road transportation, click here):

The pathway above has already been modified based on ongoing monitoring of achieved reductions, and changed circumstances in the business – we now expect a slightly different mix of techniques to hit the 2026 target, and are detailing out the concrete projects and initiatives within our Logistics division, that will fulfil the new pathway.

In brief, targets are fixed, but pathways are fluid.

A decarbonisation analyst’s work is never done

So far, so good, but the list of things we still need to do is almost as long as the list of things we’ve already done.

In an ideal world, we want every contributing area of our organisation to have a clear and actionable target in support of our decarbonisation journey. Our colleagues working in Technology & Innovation might have targets for the level of data automation, for example, in support of increasing emissions data quality and data coverage. Colleagues in commercial and operational roles might have targets for utilisation rates or empty running, that are also tracked with the overall decarbonisation efficiency target in mind.

And we still have some big areas where targets are in development, notably, parts of our scope 3 that are not related to the fuel we buy. Cecilie Damgaard Jensen, Decarbonisation Analyst points out, “The lion’s share of our emissions are in scope 1, whereas for most it’s their scope 3 – but as we continue to electrify, we’ll have more emissions in scope 2, and as the business evolves and we get more data, we see that our scope 3 is not trivial either. Although we already do a lot in practice to tackle our scope 3, and our 2050 target explicitly covers all scopes, we need to put formal interim targets in place for all scopes to empower the organisation to act – a decarbonisation analyst’s work is never done!”